Construction contractors have dampened expectations for 2026, aside from surging demand for data centers and power facilities, amid broader worries about the direction of the economy, according to “Dampened Expectations: The 2026 Construction Hiring and Business Outlook” released by the Associated General Contractors of America (AGC) and Sage.

In addition to lower expectations, contractors reported they have been impacted by tariffs, enhanced immigration enforcement, and challenges finding qualified workers.

“While there are pockets of optimism in select private-sector markets, contractors’ overall sentiment has dampened notably compared to last year,” said Jeffrey Shoaf, AGC’s Chief Executive Officer. “One reason for their lowered expectations is that contractors are increasingly worried about the broader economy, the possibility of a recession, and the outlook for materials costs.”

The report, based on nationwide survey results, measures contractors’ expectations for different market segments via a net reading — the percentage of respondents who expect the available dollar value of projects to expand compared to the percentage who expect it to shrink.

The highest net reading, 57 percent, is for data centers. Specifically, 65 percent of respondents expect the market for data center construction to increase, compared to just 8 percent who expect it to shrink. Contractors remain bullish about power projects as well, which recorded a net reading of 34 percent.

According to the survey, contractors are moderately optimistic about hospitals, other healthcare facilities, water and sewer, and manufacturing. Within healthcare, nonhospital facilities — including clinics, testing facilities, and medical labs — recorded a net reading of 24 percent, followed by hospital construction with a net reading of 20 percent. Water and sewer had a net reading of 16 percent and manufacturing posted a net reading of 15 percent.

The net reading for construction of transportation structures, such as airport and rail projects, plunged from 29 percent to 11 percent during the past year. The reading for bridge and highway construction dropped 14 percentage points to 10 percent.

Net readings declined — but remained modestly positive — for warehouse, federal work, public building, and multifamily residential projects. Expectations for contracts from federal agencies such as the U.S. General Services Administration, Department of Veterans Affairs, Army Corps of Engineers, and Naval Facilities Engineering Systems Command fell from 22 percent to 5 percent, while the multifamily residential net slid from 12 percent to 4 percent. The net for public building dropped as well, from 14 percent to 1 percent.

The net reading for K-12 construction declined from 13 percent in 2025 to minus 1 percent in this year’s survey. Higher education slipped from a net of 12 percent to minus 5 percent. Expectations for education construction have been weakening for several years, with both K-12 and higher education showing decelerating growth since 2022, aside from a brief uptick in higher education in 2024.

Expectations for lodging, private office, and retail construction were the three most negative segments in 2026. The net reading for lodging fell 14 points, from 7 percent in 2025 to minus 7 percent in this year’s survey. Private office declined by 11 points to minus 14 percent, while retail dropped 13 points to minus 18 percent.

In addition to lowered expectations, many contractors also reported impacts from new tariffs and enhanced immigration enforcement.

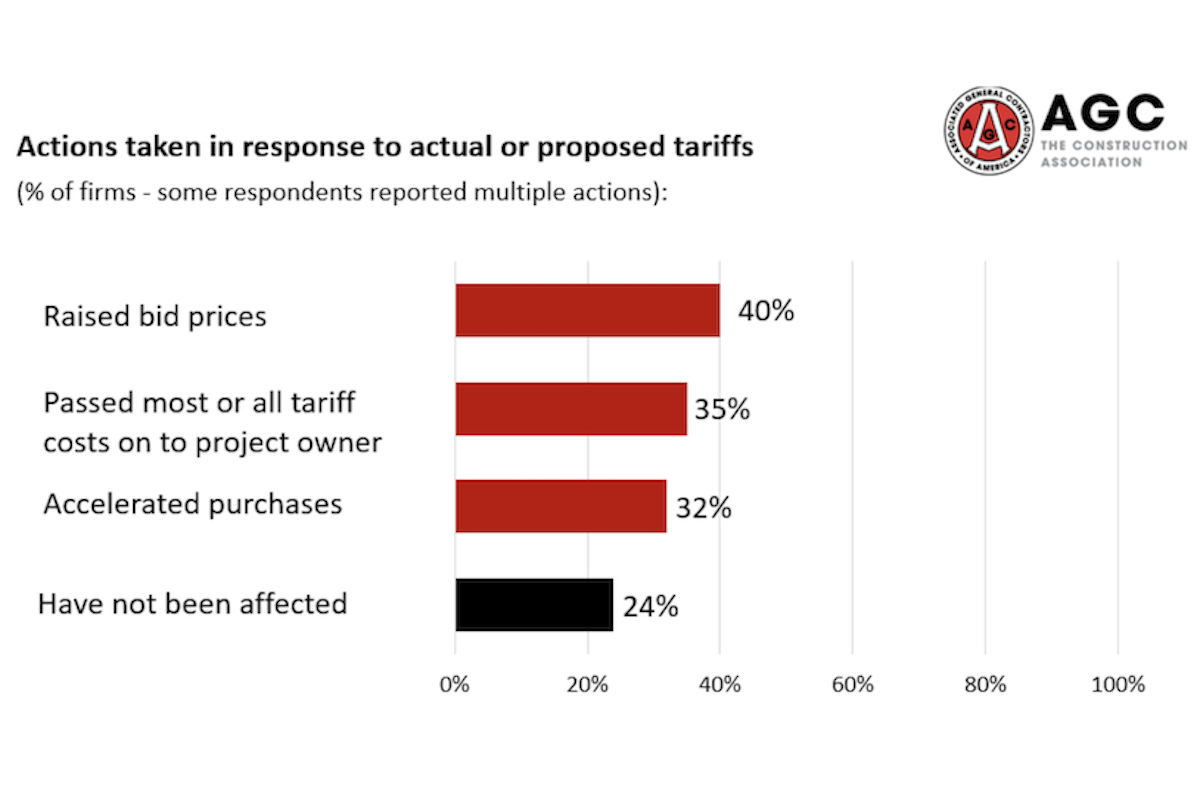

Roughly 70 percent of firms reported being affected by tariffs this year. Forty percent said they responded to actual or proposed tariffs by raising bid prices, and 20 percent of firms added price-sharing adjustments or other terms to contracts. While 35 percent reported passing most or all tariff-related costs on to project owners, 11 percent said they absorbed most or all tariff costs.

One-third of firms (33 percent) said they were affected by immigration enforcement actions in the past six months. Six percent reported a job site or off site was visited by immigration agents. Eleven percent said workers left or failed to appear because of actual or rumored immigration actions, and 24 percent reported that subcontractors lost workers.

In addition, 63 percent of respondents reported that an owner postponed or canceled a project in the past six months. When asked why, 37 percent cited a lack of funding or uncertainty about a funding source, whether federal, state, or private. Thirty-four percent said project financing was unavailable or too expensive. Just under a quarter (23 percent) of firms said increasing material or labor costs played a role.

Respondents were also asked to identify their biggest concerns for 2026. An economic slowdown or recession was the most-often mentioned concern, cited by 62 percent of firms. The next three most-cited concerns were workforce-related: 57 percent of respondents cited insufficient supply of workers or subcontractors, 56 percent selected rising direct labor costs (pay, benefits, employer taxes), and 53 percent identified worker quality.

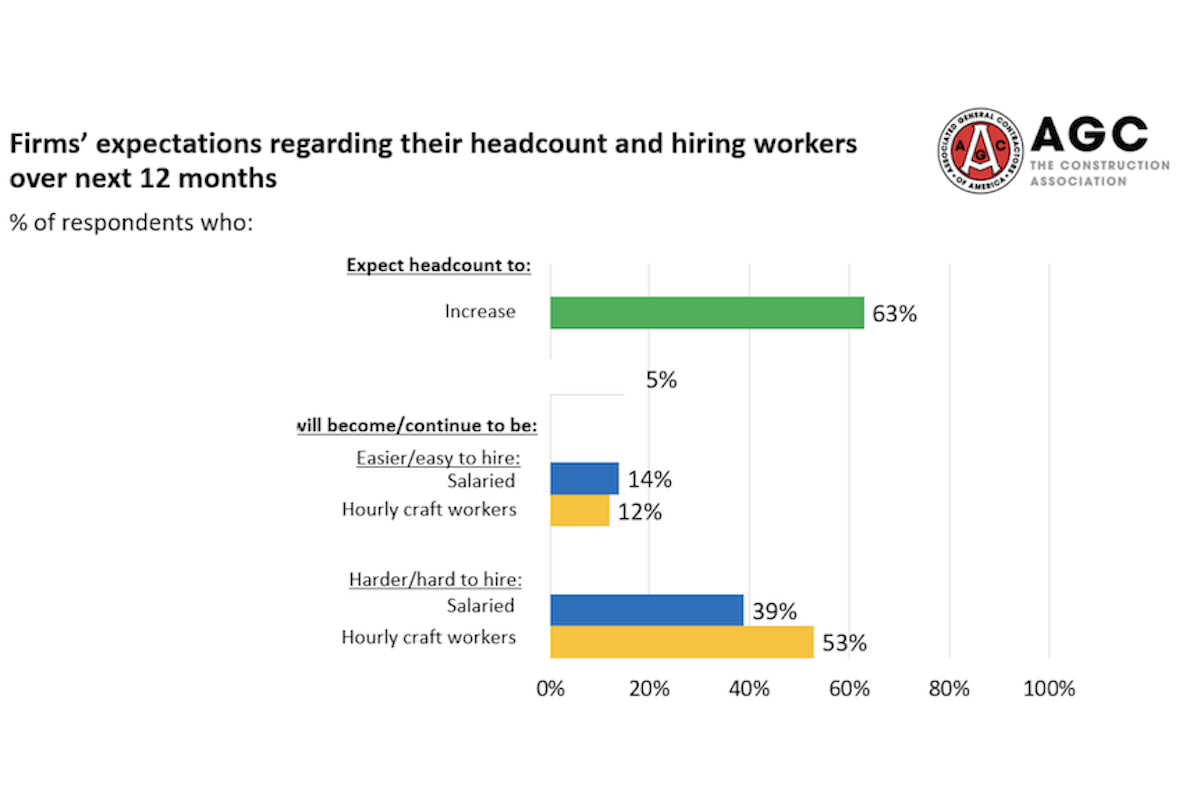

Despite those broader concerns, most firms anticipate adding workers in 2026 to meet the needs of current and planned projects. Sixty-three percent of survey respondents expect to add to their head count, compared to only 15 percent who expect a decrease. However, more than four out of five firms reported having a hard time filling hourly craft positions (82 percent) or salaried openings (80 percent) — a higher proportion than at any point in the past three years.

Officials with Sage reported that construction firms are increasingly investing in technology to address productivity and labor challenges. Sixty-one percent of respondents said their firms are using artificial intelligence (AI) or plan to increase investment in it, up from 44 percent last year. AI is most commonly used for office and administrative functions, estimating, and preconstruction activities.

“AI is becoming an increasingly important tool for construction firms facing tighter labor markets and more complex projects,” said Julie Adams, Senior Vice President of Construction and Real Estate Solutions at Sage. “Firms are using technology to improve efficiency, manage risk, and maintain productivity in a more uncertain environment.”

AGC officials said one of their top priorities this year will be to get Congress to pass a new surface transportation bill before the current one expires in September 2026. In addition, AGC said they will continue to urge the Trump administration and Congress to address workforce shortages through expanded lawful, temporary work visa programs for construction and increased investment in workforce development. They are also calling for greater clarity and restraint around tariff policy and for practical permitting reforms to reduce delays.

“With supportive infrastructure funding, workforce, trade, and permitting policies in place, construction can continue to grow the economy, deliver essential projects, and expand access to high-paying career opportunities,” Shoaf said.

The 2026 Construction Hiring and Business Outlook survey was conducted from November 4 through December 15, 2025, and drew 951 respondents from construction firms across 49 states and the District of Columbia. Participating companies represented a broad range of revenue and employment sizes. About 30 percent of respondents reported employing union workers most or all of the time, while roughly 60 percent identified as open-shop contractors.

Visit agc.org for survey results by region, state, firm size, and union or open shop.

Graphics courtesy of AGC 2026 Outlook Survey.