Evolving macroeconomic trends are shaping the financial and operational outlook of the construction sector. During CONEXPO-CON/AGG 2026, industry analysts explained the impact.

First, a fundamental shift is underway in how global trade and industrial policy are being approached, with long-standing assumptions around globalization giving way to a more strategic, state-driven framework.

Christian Lawrence, Head of Cross-Asset Strategy at RaboResearch, framed the current moment as a decisive break from past decades of economic integration, with the world transitioning away from hyper globalization to what he called “a much more protectionist, mercantilist world.”

Rather than viewing tariffs as short-term economic levers, Lawrence emphasized that they are increasingly being used as tools of geopolitical influence, particularly in the context of rising tensions between global powers.

“This is about statecraft, using economic tools for non-economic goals,” Lawrence said, pointing to a broader strategy that extends beyond trade balances.

At the center of that strategy is competition between the U.S. and China for influence and power. “The U.S. wants to remain the world’s global hegemon,” Lawrence said.

This shift is also reshaping how policymakers think about domestic manufacturing. While public discourse often focuses on jobs, Lawrence argued the real driver is capital investment and long-term positioning.

“Fast forward five to 10 years, most manufacturing might not involve that much in the way of labor,” he said.

That perspective is beginning to materialize in project pipelines, with early signs of renewed domestic investment.

“We are now starting to see manufacturing project starts pick up after a period of prolonged weakness,” Lawrence said.

Still, he cautioned that rising input costs could complicate that trajectory, particularly as energy and materials prices continue to climb.

Despite relatively strong headline economic data, Lawrence stressed that the underlying structure of the economy is becoming increasingly uneven, with growth concentrated among a narrow segment of the population and specific project types.

He described the current environment as one where aggregate numbers mask deeper imbalances. “It looks like everything’s kind of humming along quite nicely, but there are just huge cracks and uncertainty below the surface,” he said.

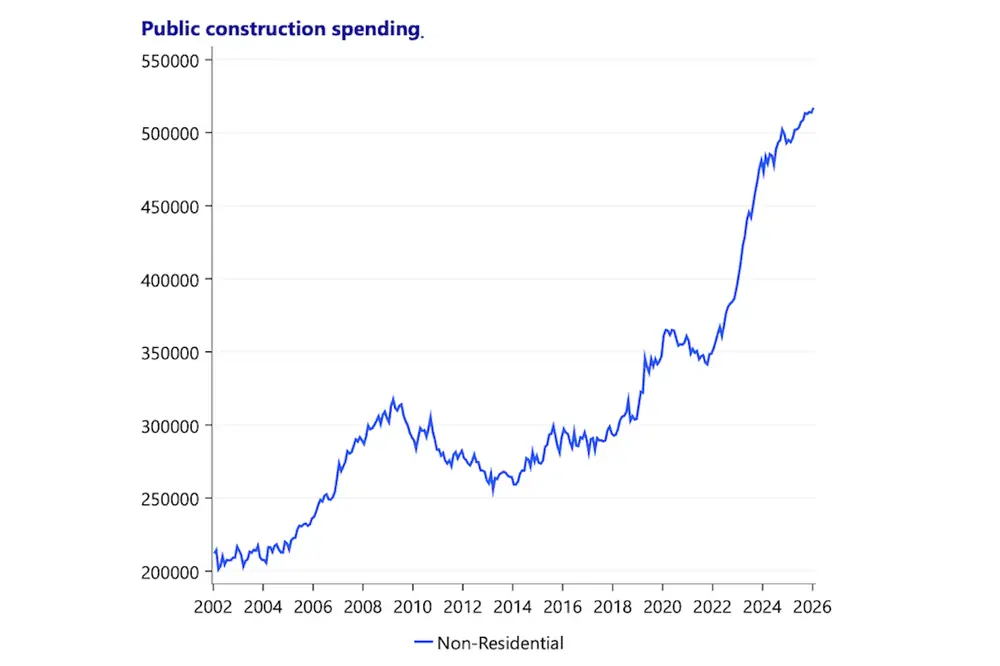

That results in a K-shaped dynamic, where some do well (the arm of the letter K reaching up) and some do not ( the arm of the letter reaching down). Lawrence sees that playing out clearly in construction, where large-scale projects continue to advance while smaller developments lag.

“Megaprojects have been absolutely booming,” he said. “Smaller projects have been somewhat more lackluster.”

Data centers, in particular, have emerged as a dominant force, driving a significant portion of current activity and shaping contractor demand.

“For the next few years, we’re still going to continue to see this trend,” Lawrence said, referencing continued investment tied to AI and digital infrastructure.

However, those strong numbers can create a misleading picture of overall market health, obscuring softness in other sectors.

“There are these pockets of things that are masking the fractures underneath,” Lawrence said.

While macroeconomic forces set the backdrop, their real impact is felt in day-to-day decisions by contractors, dealers, and equipment providers navigating cost pressures and persistent uncertainty.

Mike Ludwig, Country Sales Manager - Construction, Transportation, and Industrial at DLL, described a market that remains active but increasingly complex, with different segments reacting in different ways.

“The smaller-ticket construction projects … have still pretty much hummed along,” Ludwig said, noting that lower-cost equipment continues to move despite broader headwinds.

At the higher end of the market, however, tariffs are having a more pronounced effect, particularly on large, capital-intensive assets. Ludwig offered the example of a crane manufacturer that stopped shipping cranes to the U.S. during the tariffs.

Faced with higher costs and tighter margins, many contractors are delaying purchases and extending the life of their existing fleets, opting for maintenance over new investment in the near term. At the same time, rental demand remains strong, particularly in sectors tied to large-scale infrastructure and data center development.

Labor dynamics are adding further pressure, especially as workforce growth slows and experienced workers exit the industry.

All of those factors are felt most acutely among smaller operators, who are struggling to keep pace in an increasingly consolidated market. “The smaller, owner-operator type businesses have gotten sort of chewed up and spit out over the last couple of years,” Ludwig said.

Overlaying it all is the growing influence of artificial intelligence, which is already reshaping hiring patterns. “We certainly have seen a reduction in hiring as a result of AI developments,” Lawrence said.

Unlike past technological shifts, the speed and breadth of AI adoption present new uncertainties. Lawrence, a British citizen who recently attained American citizenship, offered a unique perspective on the meteoric rise of AI.

“The optimistic American in me says that every time a new technology comes along, everyone panics that it's going to destroy jobs, but every technology has created more jobs than it's destroyed,” he said. “The more pessimistic Brit inside me says we've never had a technology come across that has impacted so many industries so quickly.”

Reflecting on the past several years, Ludwig underscored how persistent disruption has become embedded in the operating environment. Uncertainty is no longer episodic, but structural.

“Since 2020 it’s been uncertainty every year,” Ludwig said. “I’m not really convinced that there will ever be certainty again.”

For construction stakeholders, that reality is shaping not only short-term decisions, but long-term strategy in an increasingly unpredictable market.