According to a review of federal data conducted by the American Road & Transportation Builders Association (ARTBA), states have committed federal funds to support more than 56,000 eligible transportation improvements in all 50 states during the last two years, spanning nearly every U.S. county.

The IIJA investments are funding a diverse range of highway and bridge construction, from small transportation builds to large, regional projects. According to ARTBA Chief Economist Dr. Alison Premo Black, more than 450 projects have IIJA funding of $50 million or more in the last two fiscal years, an increase of 42 percent from the previous two-year period.

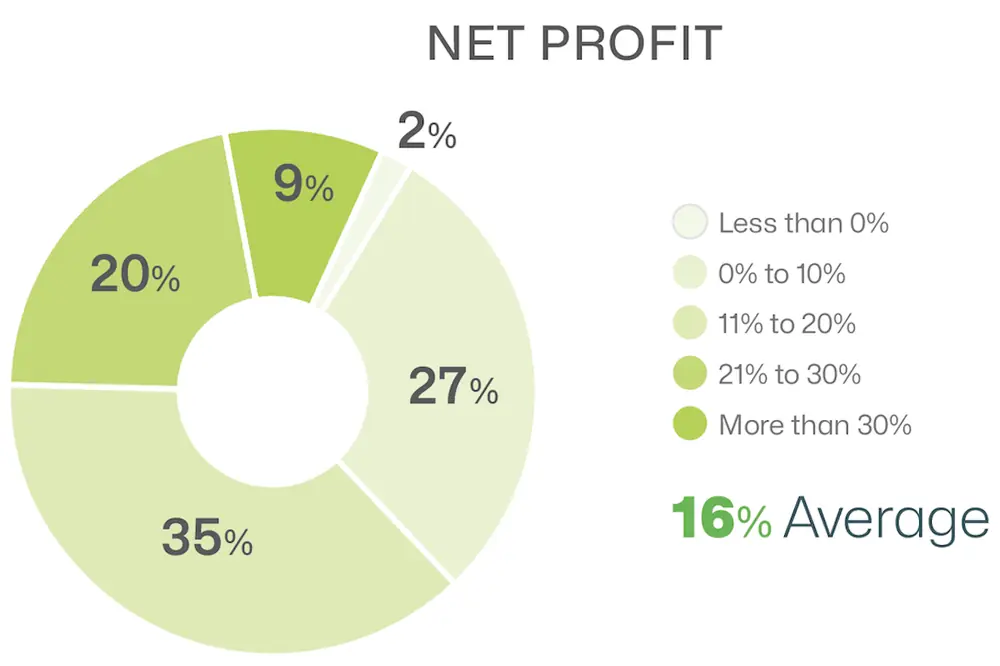

With that growth comes the challenges of finding enough labor and budgeting around changing materials costs. How can you prepare?

In FMI’s nationwide survey of respondents from a variety of construction disciplines, the Heavy Civil Construction Index declined from 56.1 in the third quarter of 2023 to 52.6 in the fourth quarter, marking the first decrease since the second quarter of 2022. All four economic measures in the survey – outlooks toward the overall economy, the economy where respondents do business, their engineering and construction (E&C) business, and E&C where they do business – weakened.

| Your local Sennebogen LLC dealer |

|---|

| ASCO Equipment |

| WPI |

| WPI |

| ASCO Equipment |

| WPI |

| ASCO Equipment |

| WPI |

| ASCO Equipment |

However, the survey indicated that contractors expected most heavy civil segments to strengthen through the end of 2023, with commercial and residential site development weakening.

The survey found that contractors continue to build backlog faster than they burn it, with only 16 percent of respondents indicating a declining backlog book/burn rate in the fourth quarter of 2023, down from 21 percent in the third quarter.

Half of all respondents said their backlog levels were significantly or somewhat higher than the fourth quarter of 2022. In fact, 76 percent of contractors reported that their backlogs were exceeding or at levels needed or expected at that point in the year. Written commentary suggested that improved project selectivity and a tight labor market contributed to healthy backlogs.

A survey conducted by Associated Builders and Contractors (ABC) also showed a slight increase in backlog from October to November 2023, inching up to 8.5 months. Despite that increase, backlog remained 0.8 months lower than at the cyclical peak in July 2023. The sharpest declines over that span occurred among contractors with more than $100 million in annual revenues, who collectively reported fewer than 10 months of backlog in November for the first time since the second quarter of 2018.

“The interest rate hikes implemented by the Federal Reserve appear to be making more of a mark on the economy,” said Anirban Basu, ABC’s Chief Economist. “Not only has the cost of capital risen over the past 20-plus months, but credit conditions are also tightening, rendering project financing even more challenging.”

Overall, total heavy civil construction put in place was expected to grow slightly more than 10 percent in 2023, according to FMI’s fourth quarter survey. Several segments – including highway and street, sewage and waste disposal, water supply, and conservation and development – were forecast to see double-digit expansion last year. Air, rail/transit, and bridges were also likely to expand in double digits with the help of IIJA funds.

For 2024, Black’s annual market outlook forecasts public highway, pavement, and street construction to grow by double digits for the second consecutive year, increasing 16 percent to $126 billion from $108.6 billion in 2023.

Two factors support that increase in construction activity, Black said. In addition to IIJA-supported projects starting construction, many states are increasing their own revenues to match federal funds and make additional transportation investments, using a combination of general fund transfers, bond issues, business taxes, and other user-fee increases.

For overall transportation construction work, including highways, ARTBA projects the total value will grow 14 percent from $187 billion in 2023 to $214 billion in 2024.

Ken Simonson, Chief Economist for Associated General Contractors of America (AGC), forecasts growth in some sectors of the industry and a decline in others.

“I expect nonresidential construction to expand in 2024, with continued strong growth for data centers and manufacturing plants, along with an increase in various types of infrastructure and power plants,” he said. “These increases should outweigh a likely decline in apartment, office, warehouse, and possibly retail and lodging construction.”

The need for labor continues to grow. According to Heather Boushey, Chief Economist for the Investing in America Cabinet, the construction industry added 2,800 jobs per month over the past year – four times the amount from 2011 to 2019, when the industry added an average of 700 jobs per month.

An ABC analysis of data released by the U.S. Bureau of Labor Statistics indicated that in November 2023, nonresidential construction employment increased by 1,400 positions on net. Heavy and civil engineering added 3,300 positions, offsetting job losses of 1,100 in nonresidential building and 800 in nonresidential specialty trade. On a year-over-year basis, construction industry employment increased by 200,000 jobs, or 2.6 percent.

The IIJA newly enabled states to invest in workforce development using their highway formula funds. More than half of states are already taking advantage of that flexibility, Boushey said.

However, “On the last day of October 2023, 5.0 percent of construction positions were unfilled, which is well above the 3.9 percent industry job opening rate observed in February 2020,” Basu said. “With nearly half of contractors intending to increase their staffing levels over the next six months, according to ABC’s Construction Confidence Index, the lack of available workers will remain a headwind for the construction industry over the next several quarters.”

Simonson agreed. “The supply of craft labor remains very tight. Wages, as measured by a Bureau of Labor Statistics series called average hourly earnings for production and nonsupervisory employees in construction, have been rising at a five to six percent annual rate for the past two years. I expect wages to go up a further five to seven percent in 2024.”

“While much of the recent decline is due to record domestic oil production and the resulting precipitous decline in gas and diesel prices, other commodities like iron and steel and lumber products are currently more affordable than they were at the same time last year,” Basu said.

Will that continue?

Simonson tracked data dating back to 2007, comparing the year-over-year change in the cost of materials used in nonresidential construction to the price contractors say they would charge to put up a set of new nonresidential buildings. In the "Cost Squeeze on Contractors" graph above, the periods in red indicate times when materials costs increased faster than bid prices, potentially squeezing contractors’ profit margins. More recently, as shown by the unshaded areas, materials prices rose less rapidly than bid prices or even declined compared to the same month a year earlier.

According to Simonson, key takeaways from that graph are:

- Materials prices have been extremely volatile in the past few years

- Bid prices do not keep up with rapid increases in materials costs

“Owners shouldn’t expect contractors to pass along materials price cuts immediately, given recent episodes or sudden sharp increases in materials costs and the prolonged period (19 months, from late 2020 to mid-2022) in which the increase in bid prices trailed the runup in materials costs,” he said.

With the industry growth Simonson expects, “I think it would be prudent to budget for four to six percent increases in materials costs,” he said.

- Started improvements on 135,800 miles of roads and launched over 7,800 bridge repair projects

- Delivered funding for 445 port and waterway projects intended to strengthen supply chains, speed up the movement of goods, lower costs, and reduce greenhouse gas emissions

- Invested in over 190 airport terminal projects, including 18 under construction and eight more already complete

- Financed over 1,200 drinking water and wastewater projects across the country, including projects that will replace hundreds of thousands of lead service lines and 651 projects to build sanitation facilities for tribal communities that lack wastewater services

- Launched over 60 projects to improve the resilience and reliability of the country’s electric grid and deliver cheaper and cleaner electricity

- States have committed federal funds to over 56,000 transportation improvements

- Nearly $100 billion in new project commitments

- 96 percent of counties have at least one project

- State DOTs are increasing capital spending by 13 percent

- Average highway construction employment is up 8 percent

- In 2023, the value of contract awards was up in 35 states

- Nearly $8 billion in road and bridge-related discretionary grant awards announced by the U.S. Department of Transporation

- In 2023, the value of contract awards was up 12 percent over 2022

- 24 percent of funds spent on new construction or added capacity

- 168 projects receiving over $100 million in federal support